.png)

At a Glance: Affordability in the GTA has genuinely improved. Average prices are down roughly 8% year-over-year, the Bank of Canada has cut its policy rate to 2.25%, and wages have outpaced inflation since 2024. Layer on a new HST rebate worth up to $130,000 on new homes, and some pre-construction properties are now priced below comparable resale. This is the corner most buyers have been waiting for.

Every market has a turning point. It is rarely the moment prices spike. It is the moment the conditions that held people back start to reverse.

For the GTA, that moment is 2026.

I want to walk you through what we are seeing on the ground, what the data says, and what it means for you if you have been sitting on the sidelines.

Affordability is driven by three forces: incomes, prices, and rates. For the first time in years, all three are moving in the buyer's favour.

Incomes are up. Canadian wages have risen roughly 4.2% year-over-year since 2024, outpacing inflation.

Prices are down. The GTA average is down about 7.1% year-over-year and close to 30% off the early 2022 peak. Detached homes, semis, and condos are all trending the same direction.

Rates are down. The Bank of Canada sits at 2.25%. Fixed mortgage rates are under 4%. That is a different world than the 5%+ fixed rates most buyers were stress-testing against two years ago.

So if affordability has genuinely improved, why have buyers not moved?

The honest answer is consumer confidence. A snap federal election, tariff uncertainty with the U.S., geopolitical instability, and a steady drip of negative headlines have kept people cautious. That caution is understandable. It is also the exact condition that creates opportunity for the buyers who are paying attention.

Demand does not disappear. It gets stored. TRREB estimates more than 100,000 sidelined buyers are ready to move. The question is when confidence returns, not if.

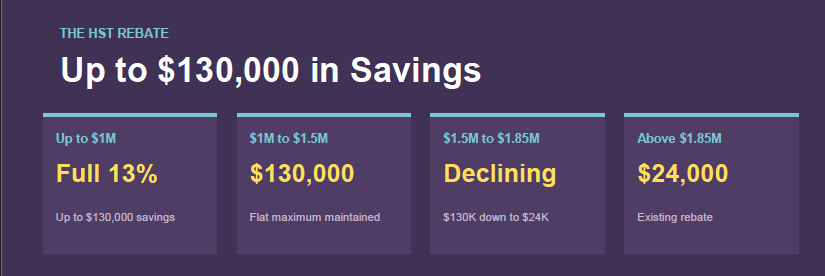

On April 1, 2026, Ontario and the federal government introduced the most significant housing incentive I have seen in my career.

Here is the structure:

The window runs April 1, 2026 to March 31, 2027. Unlike the earlier federal proposal, this applies to all buyers — first-time, repeat, and qualified rental investors. For a primary residence, construction must begin by December 31, 2028 and complete by December 31, 2031. For rental properties, the completion deadline is tighter: December 31, 2029.

One honest caveat: a lot of the fine print is still being worked out. Guidance from the federal and provincial governments has been murky. Developers, lawyers, and accountants are still working through how the rebate applies across different scenarios — assignments, rental classifications, the sliding scale between $1.5M and $1.85M, and the federal 5% portion that still requires passage of federal legislation. We expect meaningful clarity on May 1, and we will update our clients as the final rules come out.

What is not in doubt is the market response. Even with the ambiguity, the rebate has already stimulated low-rise pre-construction sales across the GTA. Developers are moving inventory that has been sitting for months. Builder sentiment has shifted for the first time in a year. Buyers who were quiet in February are on site on weekends signing paperwork.

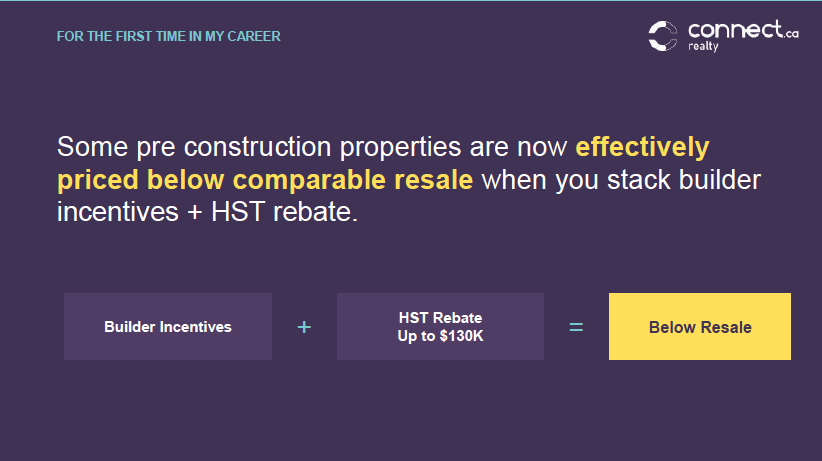

Some developers are building the discount directly into the purchase price. Others are letting you claim the rebate yourself after closing, which is particularly powerful if you are buying with a low deposit.

Either way, when you stack builder incentives on top of the HST rebate, something unusual happens: some pre-construction units are now effectively priced below comparable resale. In 20 years of doing this, I have not seen that before.

Here is the data most buyers have not fully absorbed.

In 2025, the GTA saw 5,300 new home sales — the lowest figure in 45 years of record keeping, according to BILD and Altus. A building typically needs to hit 70–80% sold before construction financing unlocks. So the majority of projects launched in the last two years will not get built.

Now look at the completion pipeline:

Year

GTHA Condo Completions

2024

~29,900

2025

~29,800

2026

~20,600 (projected, likely lower)

2027

~15,400 (projected)

2028

~12,700 (projected)

2029

~672

By 2029, new condo supply effectively falls off a cliff. Because pre-construction takes five to six years from sales launch to completion, the supply shortfall starting in 2029 is already baked in. Nothing a buyer, builder, or government does in 2026 can change it.

Meanwhile, the GTA has added roughly 2 million people since 2000 — yet 2025 sales volume (62,360) was roughly the same as sales in 2000 (60,783). Same volume. Two million more people. That is stored demand meeting a shrinking supply runway.

I want to show you a number that matters more than any market forecast.

Take a $500,000 condo purchased today with 20% down. Your monthly carrying cost is roughly $2,475. Renting that same unit costs about $2,300 per month. The difference is $175 per month, or $21,000 over 10 years.

Here is what $21,000 buys you:

The Renter's 10-year outcome: ~$320,000 paid in rent. Zero equity. Zero wealth created.

The Buyer's 10-year outcome: ~$413,000 in equity built through forced savings and appreciation.

That is roughly a 20x return on the extra cost. It is not a market call. It is math. Mortgage payments are forced savings, and forced savings are how most middle-class families build generational wealth.

My own story started with my mother taking equity from one modest property and buying my sister and me a condo when I was 20. That single decision compounded into the portfolio and the family home I own today. The vehicle was real estate. The mechanism was time.

The buyers who will look back on 2026 as the year they made the right call are not the ones waiting for a headline that says "the market is back." By the time that headline runs, prices will have already moved.

The real signal is quieter: wages up, prices down, rates down, rebate active, supply pipeline emptying. That is the corner. You do not need to call the bottom perfectly. You need to buy something you can hold, with carrying costs that make sense on your actual income, on a timeline measured in years not months.

Safety first. Building for the long term. That is how real estate wealth gets built — not in the peaks, but in the valleys nobody wanted to enter.

If you are considering a purchase in 2026, the HST rebate window closes March 31, 2027. Construction and completion deadlines are firm. The buildings that qualify are a narrower set than most buyers realize.

Book a 30-minute consultation with Ryan to walk through your numbers, review which projects qualify for the full $130,000 rebate, and map out a plan that fits your timeline and risk tolerance.