If you only follow real estate through headlines, the GTA condo market looks like a place to avoid. Condo sales fell 69% year over year in Q2 2025. New construction sales hit 28 year lows. Active listings nearly doubled. The average selling price dropped almost 6% year over year. By every surface level metric, this market looks broken.

But institutional investors aren't reading headlines. They're reading balance sheets. And they're buying.

Family offices and institutional investors have begun acquiring blocks of condos in newly completed buildings at significant discounts to original sale prices. These are off market, bulk transactions with no press releases and no fanfare. Just capital moving toward value while retail buyers step aside.

This is documented, not speculation. John Pasalis, president of Realosophy Realty and one of the most respected voices in Toronto real estate data, confirmed this shift in his June 2025 Move Smartly report. He noted that wealthy family offices and deep pocketed investors have started quietly acquiring blocks of condos at significant discounts, effectively filling the gap left by retail investors who can no longer or no longer want to close on overpriced units.

PwC's Emerging Trends in Real Estate 2026 report echoes the pattern: established players are leveraging decreased competition to make acquisitions at more favorable prices. One Toronto based fund is actively pursuing bulk condo acquisitions targeting net returns north of 18% over a two to five year horizon.

A recent Financial Post article by Garry Marr explored this same dynamic: https://financialpost.com/personal-finance/garry-marr-canada-condo-market-private-equity.

I can confirm this isn't just an academic observation. Last week, I was approached by a family office looking to acquire 20 to 40 condo units. The month before that, a group that had assembled a fund reached out about purchasing 80 to 120 units.

These aren't the large institutional players. These are smaller, nimble groups positioning early. The large scale capital hasn't fully deployed yet, but it's circling. When these groups are spending time and money assembling funds specifically to acquire GTA condos, it tells you something about what the sophisticated analysis is showing.

The answer is the supply cliff.

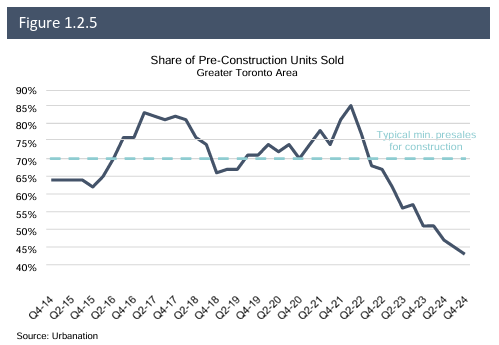

Housing starts in the GTA plummeted 60% in the first half of 2025 to levels not seen since the 1990s on a population adjusted basis. Only 1,276 condo units began construction in Q2 2025, representing an 84% decline from two years earlier. Twenty one projects representing over 4,400 units have been cancelled since 2024, and more cancellations are expected due to continued lack of presale activity.

The math is straightforward: the units not being built today are the units that won't exist in the next two to five years and beyond. And in a market where rental demand remains strong and population growth continues, the gap between future demand and future supply is exactly where institutional capital is placing its bets.

CMHC's own analysis reinforces this. Their 2025 report comparing current conditions to the 1990s concluded that Toronto's market is not overbuilt. On the contrary, they identified a structural shortage of housing that is expected to help clear any inventory buildup as the market recovers. Housing completions are projected to taper off after 2026, which combined with pent up demand, could amplify supply concerns.

RBC Economics reached a similar conclusion, anticipating that inventory could begin declining in early 2026 with conditions setting the stage for renewed activity in the second half of 2026 and more robust recovery in 2027.

There's a widespread assumption that market recoveries are slow and predictable. They rarely are. The 2008 to 2009 cycle in the GTA is a case study in how quickly conditions can change when institutional capital enters and sentiment shifts.

In January 2009, the GTA had 20,450 active listings and just 2,670 sales. That works out to 7.66 months of inventory. Prices were down over 8% year over year. Days on market had climbed to 49. Sentiment was deeply negative.

Exactly twelve months later, in January 2010, the picture was unrecognizable:

Here's the critical detail: new listings barely changed (down just 3%). Supply didn't disappear. Demand came roaring back. The buyers who waited for clarity bought at higher prices with less selection and zero negotiating power.

The entire cycle from peak fear to full recovery played out in twelve months.

I want to be clear about what this analysis does and does not suggest. The fundamentals today are different from 2009. The current inventory overhang is larger. Consumer confidence is at record lows. The correction has been deeper in certain segments, particularly sub 500 square foot investor units.

I am not predicting the same speed of recovery. But the direction of travel is supported by the data. When you combine a construction collapse of this magnitude with continued population pressure, a structural housing shortage identified by CMHC, and institutional capital that is already accumulating, the inventory that feels overwhelming today will tighten.

The question is not whether conditions improve. It is when, and whether you will be positioned when they do.

If you want to talk through what this means for your specific situation, whether you're considering entering the market, evaluating your current portfolio, or exploring financing options, that is exactly the kind of conversation I have with clients every week.