Twenty years ago, my mother bought my sister and me our first condo in Toronto. At the time, I viewed it simply as help with housing. Looking back, I realize it was one of the most strategic financial decisions anyone made on my behalf.

That first property didn't just give me a place to live. It taught me how equity accumulation works, what mortgage amortization means in practice, and how real estate can serve as a foundation for long-term wealth building. When I was ready to invest in my second property, I had equity to leverage instead of starting from scratch.

Today, I'm seeing a significant shift in the GTA market. First-time home buyer activity is up 25% compared to recent years, and a substantial portion of that growth is driven by parents helping their children enter the market. These aren't emotional purchases driven by parental guilt. They're calculated financial decisions made by investors who understand market cycles, equity growth, and the compounding effect of time in real estate.

Let's examine what the math actually shows when comparing renting versus buying over a 10-year period in the current GTA market.

As of January 2026, the average rent for a 1-bedroom condo in the GTA sits at approximately $2,300 per month, according to recent rental market data from Urbanation and TRREB. If we apply a conservative 3% annual rental increase (below the historical 4% average but realistic given current supply conditions), here's what 10 years of renting looks like:

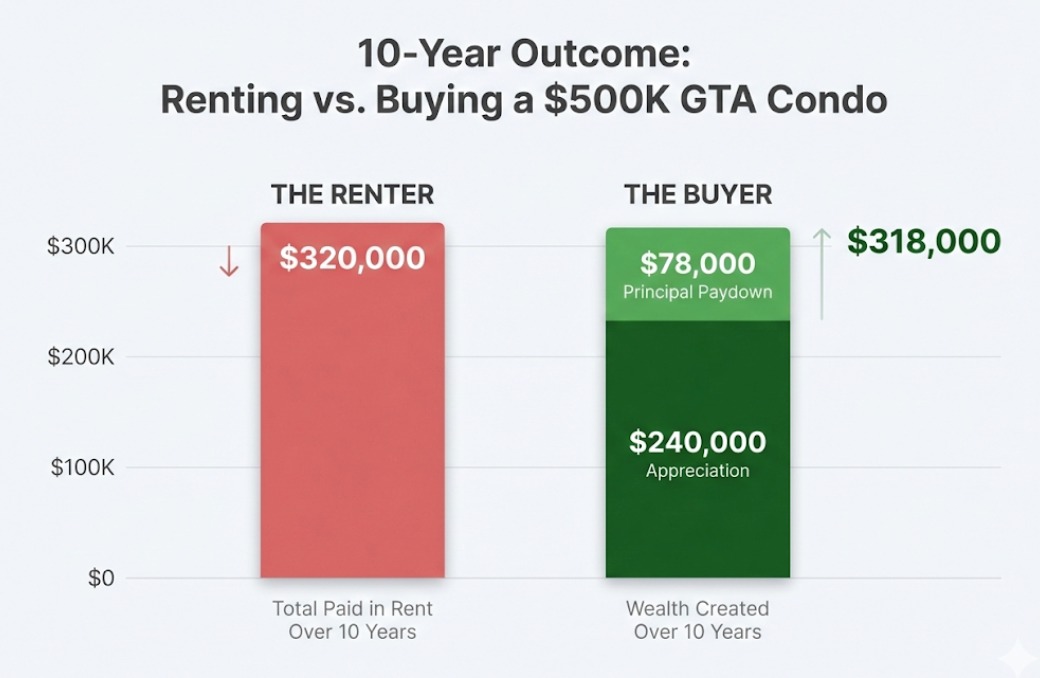

Total paid over 10 years: Approximately $320,000

Equity built: $0

Now compare that to purchasing a $500,000 1-bedroom condo in the GTA today. Current market conditions show condo prices down from peak levels, creating a more accessible entry point than we've seen in years.

At this price point, ownership costs only $175 more per month than renting initially—a far smaller premium than many parents expect. And the long-term outcome changes everything.

Total equity position: $413,000

The difference between paying $320,000 in rent with zero return versus spending marginally more ($175/month extra initially) and building over $413,000 in equity is the fundamental reason parents are making this move.

For an additional $21,000 over 10 years in monthly costs, you're creating $413,000 in equity—a 20x return on the incremental expense.

Several market factors are converging to create what many investor-parents recognize as a rare entry opportunity:

Softened Pricing: GTA condo prices have declined from peak levels reached in 2021-2022. According to TRREB data, market conditions have created more accessible entry points for buyers, particularly in the condo segment where inventory has increased.

Improved Mortgage Rates: After the Bank of Canada's rate cuts through 2024-2025, mortgage rates have stabilized in the 3.5-4% range for both variable and 5-year fixed products. While not at pandemic lows, these rates are significantly improved from the 5-6% range seen in 2023.

Strong Rental Fundamentals: Despite price softening, rental demand remains robust. TRREB reported rental transactions up 20.2% year-over-year in Q3 2025. This means if your child isn't ready to occupy the property immediately, it can generate rental income while building equity.

First-Time Buyer Activity Increasing: The 25% increase in first-time buyer activity signals market recognition that current conditions favor entry over waiting for further price declines that may not materialize.

When my mom bought that first condo for us, I didn't immediately understand the strategic value. What became clear over time was how powerful it is to start building equity early in your career rather than waiting until you've saved enough on your own.

That property taught me that real estate wealth isn't built through perfect timing or speculative flips. It's built through time in the market, consistent mortgage paydown, and the discipline to hold quality assets through normal market cycles. Starting at 23 gave me a 20-year head start that compounded in ways I couldn't have anticipated.

A few years later, when I was ready to buy my second property, I had equity to work with instead of starting from zero. Today, I own a 35-door portfolio. That first condo my mother bought was the foundation for everything that followed.

1. Assuming It Has to Be Gift vs. Loan

Many parents frame this as binary: either gift the down payment or don't help at all. There are several structures worth considering, including formal loans with repayment terms, co-ownership arrangements, or investments where the parent maintains equity position. Each has different tax implications and should be discussed with legal and tax professionals.

2. Buying Properties Children Can't Afford to Maintain

The down payment is only the beginning. Your child needs the financial stability to cover monthly mortgage payments, condo fees, property taxes, and unexpected repairs. If they can't cover these costs independently (or with rental income), the strategy creates stress instead of building wealth.

3. Ignoring the 5-7 Year Minimum Hold Period

Real estate is not a liquid asset. Transaction costs (land transfer tax, legal fees, realtor commissions) can total 5-7% of purchase price. To justify these costs and benefit from appreciation, you need to hold the property for at least 5-7 years. If your child's life situation might require selling sooner, reconsider the timing.

4. Skipping Professional Tax and Legal Guidance

The difference between structuring this as a gift, loan, co-ownership, or trust has significant tax implications for both parent and child. Land transfer tax, capital gains considerations, and principal residence exemption rules all factor into the optimal structure. This is not an area to navigate without professional advice.

5. Overlooking Location Fundamentals

Not all condos are equal investments. Proximity to transit, employment centers, universities, and amenities drives both rental demand and long-term appreciation. A cheaper condo in a weak location is rarely better than paying more for strong fundamentals.

If you're exploring this strategy for your own children, here are some helpful questions to think through:

Financial Readiness:

Timeline:

Structure:

Property Selection:

The reason first-time buyer activity is surging among parent-backed purchases isn't that parents suddenly became more generous. It's because experienced real estate investors recognize that the earlier someone enters the market, the more time they have for equity to compound.

A 25-year-old who buys their first property with parental help has a 40-year runway before traditional retirement age. Even modest 4% annual appreciation compounds dramatically over four decades. But beyond the math, there's the practical education that only comes from actual ownership.

My mother's decision to buy that first condo didn't just give me a financial head start. It gave me the foundation to build from.

As of January 2026, the GTA real estate market is experiencing what many analysts call a "normalization" after years of extreme conditions. According to TRREB, sales volumes remain below long-term averages while inventory has increased, particularly in the condo sector.

This is currently a buyer's market, which means more negotiating power for purchasers. Higher inventory levels give buyers more choice and leverage in negotiations. Sellers are more willing to consider reasonable offers, and conditions that would have been rejected outright in 2021-2022 are now being accepted.

For parents considering this strategy, these conditions create opportunity. Softer prices mean better entry points. Improved mortgage rates mean lower carrying costs than during the 2023-2024 peak rate environment.

The parents who are acting now aren't trying to time the absolute bottom. They're recognizing that current conditions offer a reasonable entry point for long-term holds, and that waiting for "perfect" conditions often means missing the opportunity entirely.

Buying real estate for your children is a financial decision that compounds over decades. It's not appropriate for every family or every situation. It requires capital, careful planning, professional guidance, and a long-term perspective.

But for families with the financial capacity and the willingness to think in 10-20 year time horizons, the math is compelling. The difference between starting at 25 versus 35 isn't just 10 years. It's the compounding effect of equity growth, forced savings through mortgage paydown, and the practical education that comes from actual ownership.

The question isn't whether real estate will appreciate. Over long enough time horizons in major metropolitan markets like the GTA, history strongly suggests it will. The question is whether your family is positioned to help your children access that appreciation curve earlier rather than later.

If you want to explore what this might look like for your specific situation, we can walk through the numbers together. The first step is understanding your goals and the available property options in today's market.

Contact us to discuss your family's real estate investment strategy.

Sources: