.jpg)

If you're trying to make sense of where the Greater Toronto Area housing market is headed, the headlines won't help you. One day it's doom and gloom; the next, someone's calling a bottom. The truth is simpler than most of what you'll read.

The GTA housing market is experiencing a historic compression: the lowest sales volume in 25 years, despite a region that has over two million more people than it did back then, and a supply pipeline that's about to run dry. These conditions don't correct overnight, but they do set the stage for what comes next.

Here's what the data actually shows and what it means for buyers and investors considering their next move.

In 2025, MLS sales across the Greater Toronto Area totalled just 62,433 transactions. That's the lowest annual total since 2000 and 26% below the 30-year average.

Here's what makes that number remarkable: the GTA now has over two million more people than it did in 2000.

Think about that for a moment. The same number of homes were sold as when the region had two million fewer residents. As a ratio of population, sales in 2025 dropped to 0.8%, the lowest level in more than 30 years. The 30-year average is 1.4%.

Why did sales fall so sharply? The reasons are well-documented:

The sales-to-new-listings ratio fell to 33%, roughly half the 30-year average of 60%, and a level we haven't seen in decades.

But here's what's easy to miss: people didn't stop needing homes. They stopped transacting temporarily. Two million more people need housing compared to the last time sales were this low. That demand is compressed, not gone. And from what I've seen, it eventually comes back to the market.

This is where the data becomes difficult to ignore.

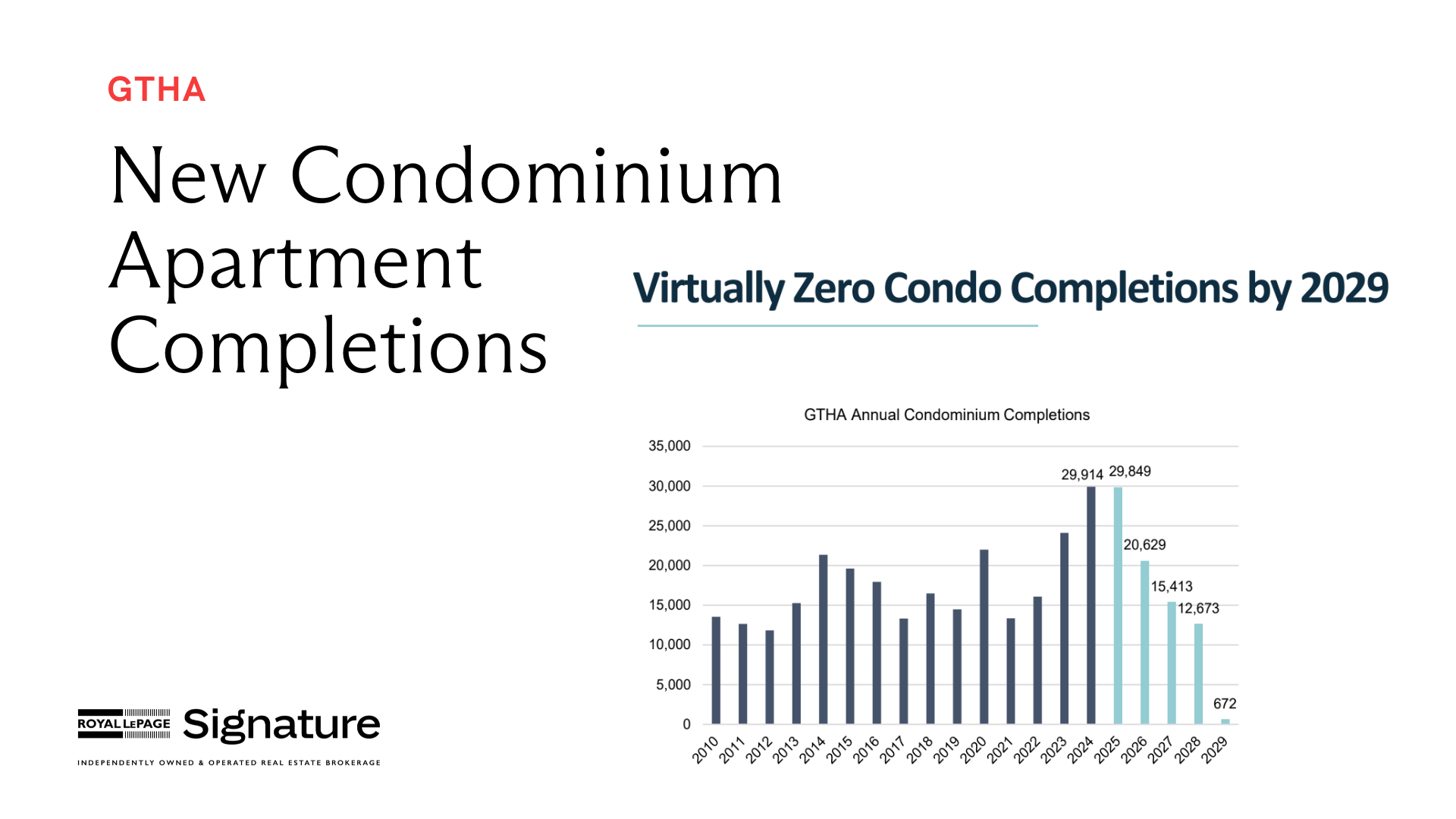

Condo completions in the GTA peaked at nearly 30,000 units in 2023 and 2024. But the pipeline is drying up fast. Completions are projected to fall to approximately 15,000 units by 2027 and under 1,000 units by 2029.

Why? Because the projects that would have delivered homes in 2027 and 2028 needed to break ground in 2024 and 2025. They didn't.

New condo sales in 2024 fell to approximately 4,590 units, a 64% decline from 2023 and the lowest volume since 1996. Construction starts dropped to their lowest level since 1998. Only a handful of new projects were launched in 2025, and even fewer sold.

Condo projects take three to five years from groundbreaking to completion. That timeline is fixed. The supply shortage for 2027-2029 isn't a forecast that might change; it's already locked in by decisions that weren't made over the past two years.

The GTA needs 25,000 to 35,000 new housing units per year to meet demand. By the end of this decade, we'll be delivering a fraction of that.

Markets don't turn all at once. They turn at the edges first, and that's what I'm starting to see.

First-time home buyers, who were priced out or spooked by rate hikes, are beginning to come off the sidelines. Improved affordability from price corrections and early rate relief is bringing some buyers back, particularly in the sub-$500K condo segment, where sales volume increased 73% in 2025.

More notably, in my conversations over the past few months with family office representatives and groups assembling capital, what I'd call the "smart money," there's growing activity. Last month, I sat across from a family office rep who manages capital for three generations of a Toronto family. He said something that stuck with me: "We're not trying to time the bottom, we're positioning for what the math tells us is coming." Institutional investors and high-net-worth buyers are acquiring assets at a discount while most of the market remains focused on today's headlines.

This isn't speculation. It's pattern recognition. Sophisticated buyers understand that the conditions creating the next tight market are forming now, even if prices haven't turned yet.

I'm not predicting that prices will spike tomorrow. Markets don't turn on a dime, and there's still uncertainty in the economy.

Now, I'll be the first to admit, there are scenarios where this plays out more slowly than I expect. If immigration targets get cut further or if rates stay elevated longer than projected, the timeline extends. But if history is any guide, the underlying math doesn't change.

The math here isn't complicated. Sales are at levels we haven't seen since 2000, yet the region has two million more people. That demand is compressed, not gone. Meanwhile, the supply cliff for 2027-2029 is already locked in; those projects needed to break ground two years ago, and they didn't. First-time buyers are starting to move, and sophisticated capital is positioning early.

When these forces eventually converge, whether that's late 2026, 2027, or beyond, the market will look very different from what it does today.

For buyers and investors, the question isn't whether you can time the exact bottom. It's whether you understand the direction this is headed and what that means for your decision.

I'm not here to tell you when to buy. But I am here to make sure you understand what the data is actually saying, so when you're ready to move, you're making that decision from a place of clarity, not headlines.